Basic Regressions with mverse

Source:vignettes/mverse_intro_regressionmodelling.Rmd

mverse_intro_regressionmodelling.RmdThis vignette describes the workflow of linear regression modeling in the multiverse with the following functions:

-

formula_branch(),add_formula_branch: create branches for regression formulas and add them to amverseobject. -

lm_mverse(): fit a simple linear model with the given formula branches and family branches. -

summary(): provide a summary of the fitted models in different branches. -

spec_curve(): display the specification curve of a model.

We will use the Boston housing dataset {Harrison Jr and Rubinfeld (1978)} as an example.

This dataset has 506 observations on 14 variables. This dataset is

extensively used in regression analyses and algorithm benchmarks. The

objective is to predict the median value of a home (medv)

with the feature variables.

dplyr::glimpse(MASS::Boston) # using kable for displaying data in html

## Rows: 506

## Columns: 14

## $ crim <dbl> 0.00632, 0.02731, 0.02729, 0.03237, 0.06905, 0.02985, 0.08829,…

## $ zn <dbl> 18.0, 0.0, 0.0, 0.0, 0.0, 0.0, 12.5, 12.5, 12.5, 12.5, 12.5, 1…

## $ indus <dbl> 2.31, 7.07, 7.07, 2.18, 2.18, 2.18, 7.87, 7.87, 7.87, 7.87, 7.…

## $ chas <int> 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0,…

## $ nox <dbl> 0.538, 0.469, 0.469, 0.458, 0.458, 0.458, 0.524, 0.524, 0.524,…

## $ rm <dbl> 6.575, 6.421, 7.185, 6.998, 7.147, 6.430, 6.012, 6.172, 5.631,…

## $ age <dbl> 65.2, 78.9, 61.1, 45.8, 54.2, 58.7, 66.6, 96.1, 100.0, 85.9, 9…

## $ dis <dbl> 4.0900, 4.9671, 4.9671, 6.0622, 6.0622, 6.0622, 5.5605, 5.9505…

## $ rad <int> 1, 2, 2, 3, 3, 3, 5, 5, 5, 5, 5, 5, 5, 4, 4, 4, 4, 4, 4, 4, 4,…

## $ tax <dbl> 296, 242, 242, 222, 222, 222, 311, 311, 311, 311, 311, 311, 31…

## $ ptratio <dbl> 15.3, 17.8, 17.8, 18.7, 18.7, 18.7, 15.2, 15.2, 15.2, 15.2, 15…

## $ black <dbl> 396.90, 396.90, 392.83, 394.63, 396.90, 394.12, 395.60, 396.90…

## $ lstat <dbl> 4.98, 9.14, 4.03, 2.94, 5.33, 5.21, 12.43, 19.15, 29.93, 17.10…

## $ medv <dbl> 24.0, 21.6, 34.7, 33.4, 36.2, 28.7, 22.9, 27.1, 16.5, 18.9, 15…Simple Linear Regression with mverse

In order to perform a linear regression in the multiverse, we create

a formula branch with all the models we wish to explore, add it the

mverse object, and execute lm on each universe

by calling lm_mverse.

Create a multiverse with mverse.

mv <- create_multiverse(MASS::Boston)We can explore models of the median value of home prices

medv on different combinations of the following explanatory

variables: proportion of adults without some high school education and

proportion of male workers classified as laborers (lstat),

average number of rooms per dwelling (rm), per capita crime

rate (crim), and property tax (tax).

Create the models with formula_branch()

formulas <- formula_branch(medv ~ log(lstat) * rm,

medv ~ log(lstat) * tax,

medv ~ log(lstat) * tax * rm)Add the models to the multiverse mv.

mv <- mv |> add_formula_branch(formulas)Fit lm() across mv using

lm_mverse().

lm_mverse(mv)By default, summary will give the estimates of

parameters for each model. You can also output other information by

changing the output parameter.

summary(mv)

## # A tibble: 16 × 10

## universe formulas_branch term estimate std.error statistic p.value conf.low

## <fct> <fct> <chr> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 1 formulas_1 (Int… -2.49e+1 6.66 -3.74 2.07e- 4 -3.80e+1

## 2 1 formulas_1 log(… 1.16e+1 2.61 4.45 1.05e- 5 6.50e+0

## 3 1 formulas_1 rm 1.10e+1 0.973 11.3 2.08e-26 9.05e+0

## 4 1 formulas_1 log(… -3.35e+0 0.405 -8.29 1.04e-15 -4.15e+0

## 5 2 formulas_2 (Int… 4.62e+1 2.83 16.3 1.89e-48 4.07e+1

## 6 2 formulas_2 log(… -9.60e+0 1.15 -8.31 9.04e-16 -1.19e+1

## 7 2 formulas_2 tax 1.35e-2 0.00750 1.80 7.23e- 2 -1.23e-3

## 8 2 formulas_2 log(… -6.35e-3 0.00278 -2.28 2.29e- 2 -1.18e-2

## 9 3 formulas_3 (Int… -1.88e+2 15.4 -12.2 3.36e-30 -2.18e+2

## 10 3 formulas_3 log(… 5.23e+1 6.70 7.80 3.73e-14 3.91e+1

## 11 3 formulas_3 tax 3.82e-1 0.0344 11.1 7.46e-26 3.15e-1

## 12 3 formulas_3 rm 3.10e+1 2.30 13.5 1.98e-35 2.65e+1

## 13 3 formulas_3 log(… -1.00e-1 0.0135 -7.40 5.89e-13 -1.27e-1

## 14 3 formulas_3 log(… -7.30e+0 1.06 -6.86 2.04e-11 -9.40e+0

## 15 3 formulas_3 tax:… -4.84e-2 0.00529 -9.16 1.32e-18 -5.88e-2

## 16 3 formulas_3 log(… 1.07e-2 0.00216 4.96 9.62e- 7 6.49e-3

## # ℹ 2 more variables: conf.high <dbl>, formulas_branch_code <fct>Changing output to df yields the degrees of

freedom table.

summary(mv, output = "df")

## universe formulas_branch p n.minus.p p.star formulas_branch_code

## 1 1 formulas_1 4 502 4 medv ~ log(lstat) * rm

## 2 2 formulas_2 4 502 4 medv ~ log(lstat) * tax

## 3 3 formulas_3 8 498 8 medv ~ log(lstat) * tax * rmOther options include F (output = "f") statistics

summary(mv, output = "f")

## universe formulas_branch value numdf dendf formulas_branch_code

## 1 1 formulas_1 482.2512 3 502 medv ~ log(lstat) * rm

## 2 2 formulas_2 341.0488 3 502 medv ~ log(lstat) * tax

## 3 3 formulas_3 367.7342 7 498 medv ~ log(lstat) * tax * rmand

(output = "r").

# output R-squared by `r.squared` or "r"

summary(mv, output = "r")

## universe formulas_branch r.squared adj.r.squared formulas_branch_code

## 1 1 formulas_1 0.7423994 0.7408600 medv ~ log(lstat) * rm

## 2 2 formulas_2 0.6708513 0.6688842 medv ~ log(lstat) * tax

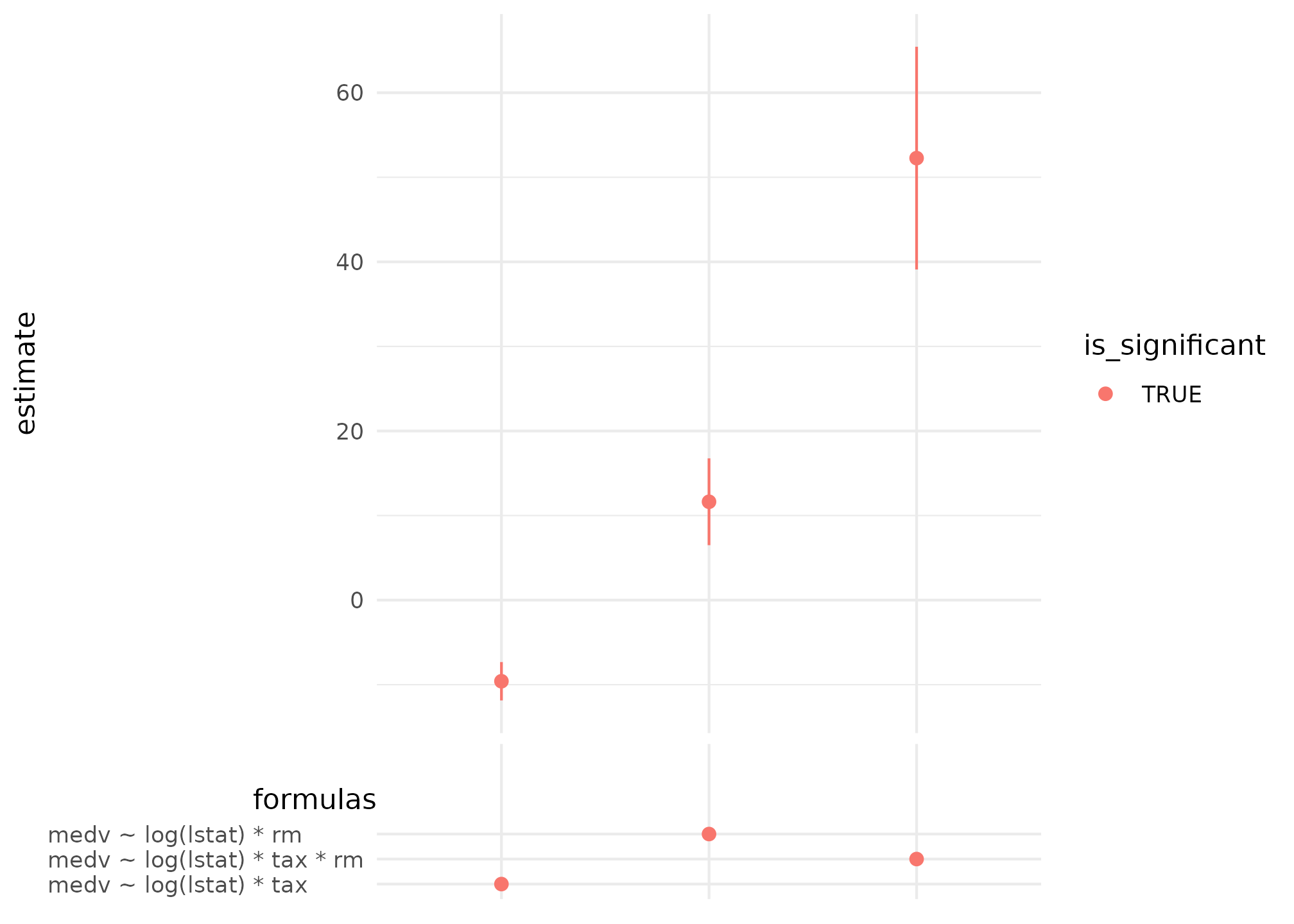

## 3 3 formulas_3 0.8378980 0.8356194 medv ~ log(lstat) * tax * rmFinally, we can display how the effect of number of rooms in a

dwelling log(lstat) using spec_curve.

spec_summary(mv, var = "log(lstat)") |>

spec_curve(label = "code") +

ggplot2::labs("Significant at 0.05")